Insurance adjuster duties: what 87% of homeowners miss

You file a claim after a burst pipe floods your home, and the adjuster arrives within days. Many homeowners assume this professional works for them, advocating for maximum coverage and fast payment. The reality is different. Insurance adjusters serve the insurance company, investigating claims to determine coverage, estimate costs, and recommend settlements. Understanding their true responsibilities helps you navigate water or fire damage claims in Northeast Sacramento with confidence, ensuring you document losses properly and communicate effectively throughout the process.

Table of Contents

- Key takeaways

- How insurance adjusters investigate and assess claims

- Specifics of water damage claims and adjuster roles in California

- Understanding fire damage adjustment and multi-peril complexities

- Types of insurance adjusters and regulatory requirements in California

- How PuroClean supports your insurance claims process

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Adjusters serve insurers | They investigate claims to determine coverage, estimate repair costs, and recommend settlements for the insurer. |

| Sudden vs gradual loss | Water damage coverage hinges on whether the loss was sudden rather than gradual, with sudden events typically covered. |

| California claim timelines | California regulations require adjusters to acknowledge and decide claims within set timeframes. |

| Adjuster types vary | Some adjusters work for insurers while others serve homeowners with different priorities. |

| Document everything | Provide photos, measurements, and eyewitness statements to support the claim and aid evaluation. |

How insurance adjusters investigate and assess claims

Insurance adjusters investigate claims by inspecting damage, gathering evidence like photos and statements, determining coverage under policy terms, estimating repair costs using tools like Xactimate, and recommending settlements. This process follows a structured approach designed to verify losses and calculate fair compensation. When an adjuster arrives at your property, they document every detail that supports or challenges your claim.

The investigation starts with a thorough walkthrough. Adjusters photograph damaged areas, measure affected spaces, and note the extent of destruction. For water damage, they check walls, floors, ceilings, and hidden spaces like crawlspaces where moisture may have spread. They collect statements from you about how the damage occurred, when you discovered it, and what emergency steps you took. These statements help establish the timeline and cause.

Adjusters then review your policy to determine what coverage applies. Not all damage falls under standard homeowners policies. They compare the documented loss against your policy’s declarations page, exclusions, and endorsements. This step separates covered perils from excluded ones. For example, a sudden pipe burst typically qualifies, while long-term seepage from a slow leak does not.

Cost estimation relies on specialized software. Most adjusters use Xactimate, an industry-standard platform that calculates repair costs based on local labor rates, material prices, and standard construction practices. The software generates detailed line-item estimates covering demolition, drying, reconstruction, and finishing work. These estimates form the basis for settlement offers.

Pro Tip: Request a copy of the adjuster’s estimate and compare it against quotes from licensed contractors. Discrepancies in scope or pricing can be negotiated if you provide documentation supporting higher costs.

After completing the investigation, adjusters compile their findings into a report for the insurance company. This report includes photos, measurements, cost estimates, policy analysis, and a recommended settlement amount. The insurer reviews this recommendation and issues a decision. Understanding this process helps you prepare documentation, answer questions accurately, and recognize when insurance claims require additional support from restoration professionals.

Specifics of water damage claims and adjuster roles in California

For water damage in California homeowners policies, adjusters distinguish sudden/accidental losses like burst pipes (covered) from gradual leaks or floods (excluded), must document cause with plumber reports, and apply IICRC S500 drying standards. This distinction determines whether your claim receives approval or denial. California policies typically cover water damage from internal plumbing failures, appliance malfunctions, and roof leaks during storms, but exclude damage from rising water, surface runoff, or long-term moisture intrusion.

Adjusters look for evidence of suddenness. A pipe that bursts overnight qualifies as sudden. A toilet supply line that fails while you’re at work meets the standard. However, a bathroom floor rotted from months of unnoticed leaks does not. The adjuster will ask when you first noticed the problem, what maintenance you performed, and whether any prior issues existed. Honest answers matter because inconsistencies can delay or derail claims.

Documentation becomes critical in water damage cases. Adjusters often require plumber reports that identify the failure point, explain the cause, and confirm the damage timeline. These reports provide third-party verification that supports your claim narrative. Without them, adjusters may question whether damage occurred suddenly or developed gradually. Keep all invoices, repair estimates, and professional assessments organized for easy submission.

California adjusters must follow industry standards for water damage mitigation. The IICRC S500 Standard provides guidelines for water extraction, structural drying, and moisture monitoring. Adjusters verify that restoration work meets these standards to prevent future mold growth and structural issues. They check drying equipment placement, humidity readings, and moisture meter logs. Proper adherence to S500 protects both you and the insurer from secondary damage claims.

Pro Tip: Start water extraction and drying immediately after damage occurs. Delaying mitigation can lead to mold growth within 24 to 48 hours, and insurers may reduce payouts if you fail to prevent additional damage.

| Water damage type | Typical coverage status | Documentation required |

|---|---|---|

| Burst pipe | Covered | Plumber report, photos, drying logs |

| Appliance failure | Covered | Appliance age, maintenance records |

| Roof leak (storm) | Covered | Roofing inspection, weather reports |

| Gradual seepage | Excluded | N/A (claim denied) |

| Flood/surface water | Excluded (NFIP required) | N/A (separate flood policy needed) |

California law also mandates timelines for claim processing. After you submit proof of loss, adjusters must complete investigations promptly. Most water damage claims resolve within 30 to 60 days if documentation is complete and coverage is clear. Complex cases involving disputes over cause or extensive damage may take longer. Understanding these timelines helps you plan temporary housing, coordinate repairs, and manage expectations. If you need residential mold and property restoration services, starting the process early ensures faster recovery.

Understanding fire damage adjustment and multi-peril complexities

Fire damage adjustment includes structural assessment, smoke and soot damage evaluation, water from suppression efforts, contents inventory, cause and origin investigation, and code upgrades, using Xactimate for scopes. Fire claims involve multiple damage types that require specialized knowledge. Adjusters must account for flames that destroy framing, smoke that permeates walls and belongings, and water that firefighters use to extinguish the blaze. Each element adds complexity to the investigation and settlement calculation.

The fire damage adjustment process follows these steps:

- Secure the property and assess safety hazards like structural instability or electrical risks.

- Document the fire’s origin and cause through investigation, often involving fire department reports and forensic analysis.

- Inventory all damaged contents, separating items that can be cleaned from those requiring replacement.

- Evaluate structural damage to framing, roofing, walls, and foundations, noting areas needing demolition or repair.

- Assess smoke and soot damage throughout the property, including areas not directly touched by flames.

- Calculate water damage from firefighting efforts, which often saturates insulation, drywall, and flooring.

- Review code and ordinance coverage for mandatory upgrades required during reconstruction.

Smoke and soot create hidden damage that extends far beyond burned areas. Soot particles infiltrate HVAC systems, settle on surfaces throughout the home, and embed in porous materials like drywall and insulation. Adjusters inspect every room, not just fire-damaged zones, to identify smoke migration patterns. They note odor intensity, discoloration, and residue buildup. Cleaning or replacing these affected materials adds significant costs to claims.

Water damage from firefighting complicates adjustments. Hundreds or thousands of gallons soak floors, walls, and ceilings during fire suppression. This water causes swelling, warping, and potential mold growth if not dried quickly. Adjusters treat this water damage as part of the fire claim, not a separate water loss. They document moisture levels, recommend drying protocols, and include water mitigation costs in their estimates.

Pro Tip: Take detailed photos and videos of all damaged contents before cleanup begins. Adjusters need visual evidence to verify losses, and early documentation prevents disputes over item condition or value.

| Damage component | Adjustment considerations | Common challenges |

|---|---|---|

| Structural fire damage | Framing, roofing, load-bearing walls | Determining repair vs rebuild costs |

| Smoke and soot | HVAC cleaning, surface restoration, odor removal | Proving extent in non-burned areas |

| Water from suppression | Drying, demolition, mold prevention | Separating fire water from other sources |

| Contents inventory | Valuation, depreciation, replacement | Documenting pre-loss condition and value |

| Code upgrades | Mandatory improvements during reconstruction | Coverage limits under ordinance provisions |

Code and ordinance coverage becomes essential in fire claims. When you rebuild after a fire, local building codes may require upgrades like new electrical systems, seismic reinforcements, or energy-efficient materials. Standard policies often include limited coverage for these mandated improvements, but it may not cover full costs. Adjusters evaluate which upgrades apply and calculate coverage under your policy’s ordinance provisions. If your policy lacks adequate code upgrade coverage, you may face out-of-pocket expenses.

Multi-peril situations arise when fire and water damage overlap. A kitchen fire that triggers sprinklers creates both fire and water losses in a single event. Adjusters must separate covered perils from excluded ones while accounting for all damage sources. They coordinate with fire investigators, restoration contractors, and engineers to build comprehensive scopes. This complexity extends claim timelines but ensures accurate settlements. Homeowners benefit from starting fire damage restoration services quickly to prevent further deterioration while adjusters complete their investigations.

Types of insurance adjusters and regulatory requirements in California

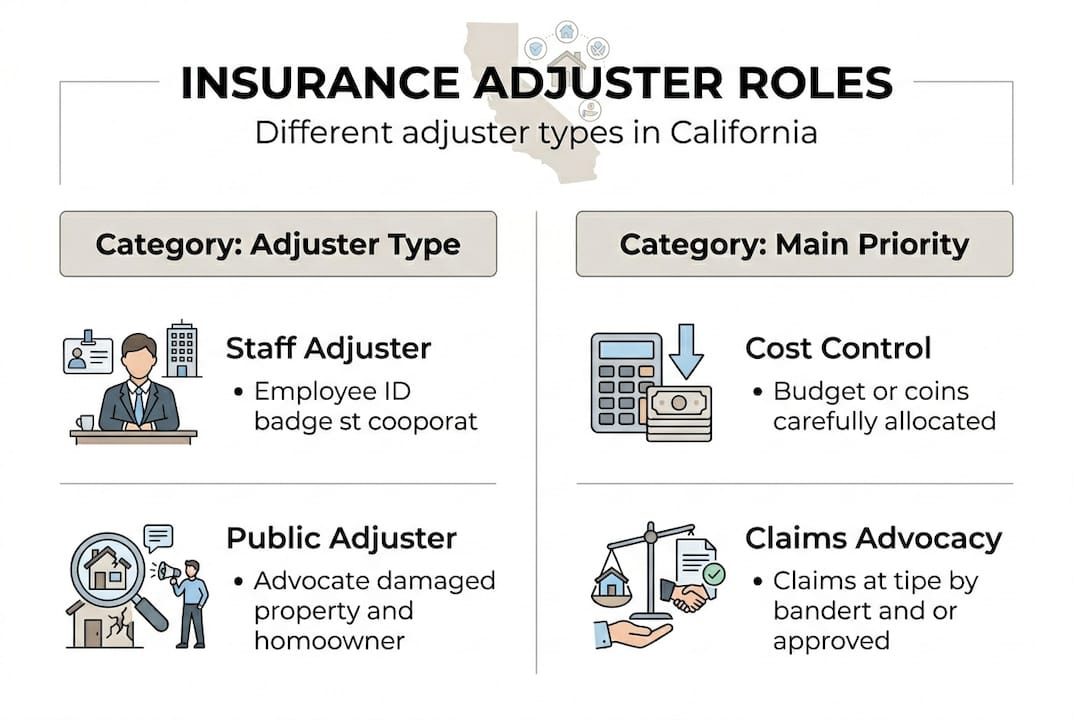

Three types of adjusters handle property claims. Staff adjusters work directly for insurance companies as salaried employees. Independent adjusters contract with multiple insurers on a per-claim basis, often during high-volume periods like natural disasters. Public adjusters represent policyholders, not insurers, and charge fees based on settlement amounts. Each type operates under different incentives and priorities.

Staff adjusters focus on controlling claim costs for their employer while maintaining customer satisfaction. They handle routine claims efficiently and follow company protocols closely. Independent adjusters bring flexibility during catastrophic events when staff adjusters are overwhelmed. They work for multiple insurers simultaneously and may handle hundreds of claims after major disasters. Public adjusters advocate exclusively for homeowners, investigating losses, preparing documentation, and negotiating with insurers to maximize settlements. Studies show public adjusters can increase settlements by 40% to 700% compared to homeowner-negotiated amounts, though they typically charge 5% to 15% of the final payout.

California CDI regulations mandate adjusters contact within specified times, thorough inspections including attics and crawlspaces, Fair Claims Practices with 15-day acknowledgment and 40-day decisions, and training on disasters. These requirements protect homeowners from delayed or inadequate claim handling. After you report a loss, your insurer must acknowledge receipt within 15 days. Once you submit all required documentation, the insurer must accept or deny the claim within 40 days.

Thorough inspections are non-negotiable. Adjusters must examine all potentially damaged areas, including spaces homeowners might overlook. For water damage, this means checking attics for roof leaks, crawlspaces for plumbing failures, and wall cavities for hidden moisture. For fire damage, it includes inspecting HVAC ducts for smoke residue and examining structural members for heat damage. Incomplete inspections lead to underpaid claims and future disputes.

Pro Tip: If an adjuster skips areas you believe are damaged, politely request they inspect those spaces and document the request in writing. California regulations require comprehensive assessments, and you can file complaints with the Department of Insurance if adjusters cut corners.

| Adjuster type | Works for | Payment structure | Typical priorities | |—|—|—| | Staff adjuster | Insurance company (employee) | Salary | Efficient claim resolution, cost control, customer service | | Independent adjuster | Insurance company (contractor) | Per-claim fee | High-volume processing, meeting insurer standards | | Public adjuster | Policyholder | Percentage of settlement (5-15%) | Maximizing claim payout, thorough documentation |

California also requires adjusters to complete training on disaster-related claims. After major events like wildfires or floods, adjusters must understand specific coverage issues, local building codes, and emergency response protocols. This training ensures adjusters can handle complex losses competently. Homeowners in Northeast Sacramento benefit from these standards, knowing local adjuster practices must meet state requirements for thoroughness and timeliness.

Fair Claims Practices regulations extend beyond timelines. Adjusters cannot misrepresent policy terms, refuse to pay claims without reasonable investigation, or require unnecessary documentation. If you suspect unfair treatment, document all communications and file a complaint with the California Department of Insurance. The department investigates violations and can penalize insurers for non-compliance. Understanding your rights under these regulations empowers you to hold adjusters accountable and ensures your claim receives fair consideration.

How PuroClean supports your insurance claims process

Navigating insurance claims after water or fire damage can feel overwhelming, especially when you’re managing displaced family members and coordinating repairs. PuroClean of Northeast Sacramento specializes in emergency restoration services that support your claim process from start to finish. Our team documents damage thoroughly, follows industry standards like IICRC S500, and provides detailed reports that adjusters need to process claims accurately.

We respond 24/7 to water emergencies, extracting standing water, drying structures, and preventing secondary damage that could complicate your claim. Our fire damage restoration services address smoke, soot, and water from suppression efforts, ensuring comprehensive recovery. If moisture leads to mold growth, our mold mitigation and removal services eliminate contamination safely. Working with certified professionals protects your property and strengthens your insurance claim. Contact PuroClean of Northeast Sacramento today to start your restoration with confidence.

Frequently asked questions

What are the key responsibilities of an insurance adjuster?

Insurance adjusters investigate claims by inspecting damage, gathering evidence through photos and statements, reviewing policy coverage to determine what qualifies, estimating repair costs using industry software, and recommending settlement amounts to the insurance company. They serve the insurer, not the homeowner, focusing on accurate loss assessment within policy terms.

How do insurance adjusters differentiate between sudden and gradual water damage?

Adjusters classify sudden water damage like burst pipes or appliance failures as covered perils because they occur unexpectedly. Gradual water damage from long-term leaks, poor maintenance, or slow seepage is excluded because policies require homeowners to prevent progressive deterioration. Plumber reports and damage timelines help adjusters make this determination.

What is the typical timeline for an insurance adjuster to process fire damage claims?

Fire damage claims typically take six to eighteen months to resolve due to complexity involving structural assessment, contents inventory, smoke damage evaluation, and code upgrade requirements. California regulations require adjusters to acknowledge claims within 15 days and decide within 40 days after receiving complete documentation, though investigations may extend timelines for complicated losses.

Why might a homeowner consider hiring a public adjuster?

Public adjusters work exclusively for homeowners, not insurance companies, advocating for maximum settlements through thorough documentation and negotiation. Research indicates public adjusters can increase claim payouts by 40% to 700% compared to homeowner-negotiated amounts. They charge fees of 5% to 15% of the final settlement, which can be worthwhile for large or disputed claims.

Recommended

- Restoration and Insurance Claims: What Homeowners Need to Know – PuroClean of Northeast Sacramento

- Fire Damage Assessment: Key Steps for Recovery – PuroClean of Northeast Sacramento

- Why Hire Restoration Services After Property Damage – PuroClean of Northeast Sacramento

- Why Hire Restoration Services After Property Damage – PuroClean of Northeast Sacramento