Parametric insurance in New York allows payouts based on measurable storm data like wind speed or rainfall but for Newburgh homeowners, the bigger risk is how quickly storm damage spreads before any insurance payment is made.

For homeowners in Newburgh and throughout the Hudson Valley including areas like Poughkeepsie and Fishkill, storm damage doesn’t just depend on the event itself, but how quickly action is taken afterward. New York’s parametric insurance law lets some homeowners get payouts based on storm data like wind speed or rainfall but it doesn’t change how fast damage spreads through your Newburgh home once water gets inside.

This guide is written for homeowners in Newburgh, NY, and the surrounding Hudson Valley communities including Poughkeepsie, Fishkill, Beacon, and New Windsor where storm‑driven roof damage, winter leaks from ice dams, and hidden moisture in older homes are common.

Key Takeaways for Newburgh Homeowners

- Parametric insurance in New York may trigger payouts based on storm data, not just visible damage

- It does not replace traditional homeowners insurance

- Storm damage begins immediately and can escalate within 24–72 hours

- Moisture spreads beyond visible areas, increasing risk of mold and structural damage

- Acting quickly after a storm is what determines the severity and cost of repairs

What New York’s parametric insurance law means for Newburgh NY homeowners

Parametric insurance is a type of coverage where payouts are triggered by measurable events—like wind speed, rainfall, or air pressure but rather than only documented property damage. New York now recognizes parametric insurance for personal‑lines policies, which means some homeowners in Newburgh can begin to see coverage tied to storm‑data thresholds, not just visible damage.

What the New York law actually says

New York’s amendment to Insurance Law §1113 allows parametric insurance, which means coverage can be triggered by measurable storm data, not just visible property damage. Parametric insurance is defined by three core elements:

- Payment is based on a measurable event (like wind speed or rainfall levels)

- That event is verified by a third‑party data source (such as weather stations or approved providers)

- The payout is tied to predefined thresholds, not traditional inspections

The key distinction: this law does not guarantee automatic payouts, and it does not eliminate the possibility of adjusters. It introduces a different way claims may be triggered. What changes here isn’t coverage, it’s timing. Parametric insurance is now recognized as an authorized type of personal‑lines coverage under New York Insurance Law §1113.

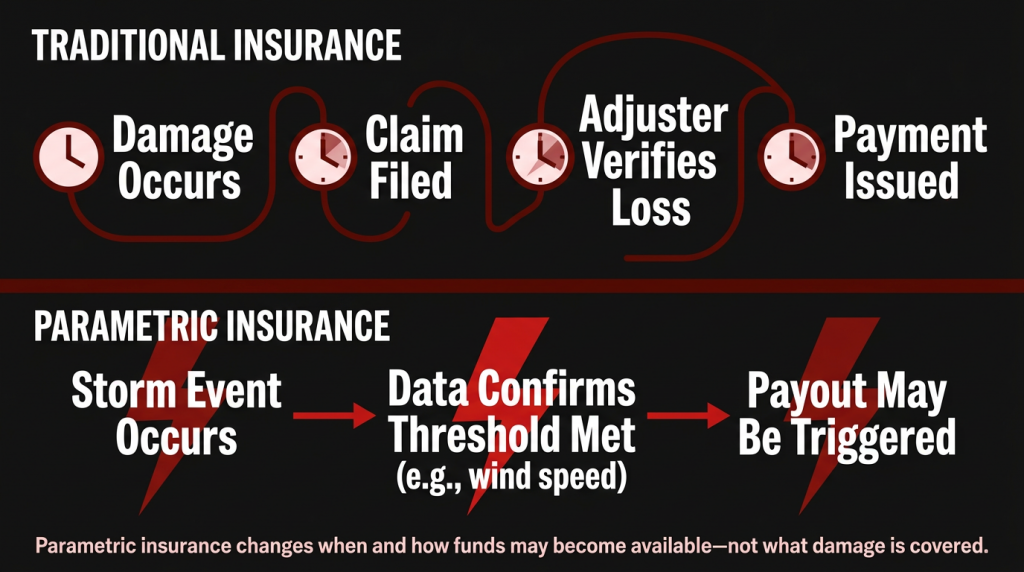

How parametric insurance changes the claims timeline

Parametric insurance changes when and how funds may become available after a storm—not what damage is covered. Traditional insurance typically follows this path:

- Damage occurs

- A claim is filed

- An adjuster verifies the loss

- Payment is issued

Parametric insurance introduces a different sequence:

- A storm event occurs

- Data confirms a threshold was met (e.g., wind speed)

- A payout may be triggered based on that event, depending on the policy

This means money can potentially move faster but only if the event meets defined criteria. For example: if a policy includes a wind trigger of 55 mph, a storm like the one that impacted Fishkill in March could meet that threshold, depending on how the policy is structured and which data source is used.

Why one storm creates multiple layers of damage

A single storm doesn’t cause one problem in a structure, it creates a chain reaction that escalates without immediate action. Here’s what happens in real homes across Newburgh and the Hudson Valley:

- Wind damage compromises the roof

Shingles lift, flashing separates, or debris punctures the structure. - Rain enters the home

Water travels beyond the entry point—down rafters, into insulation, across ceilings, and behind walls. - Power loss stops mitigation

Without electricity, professional drying equipment—air movers, dehumidifiers, and filtration systems—can’t run. - Humidity spikes rapidly

Indoor moisture levels can reach 80–90% in a closed structure. - Damage escalates

What started as a clean water intrusion can evolve into contamination and structural degradation within days.

What matters most here is not the initial damage—it’s how quickly it spreads.

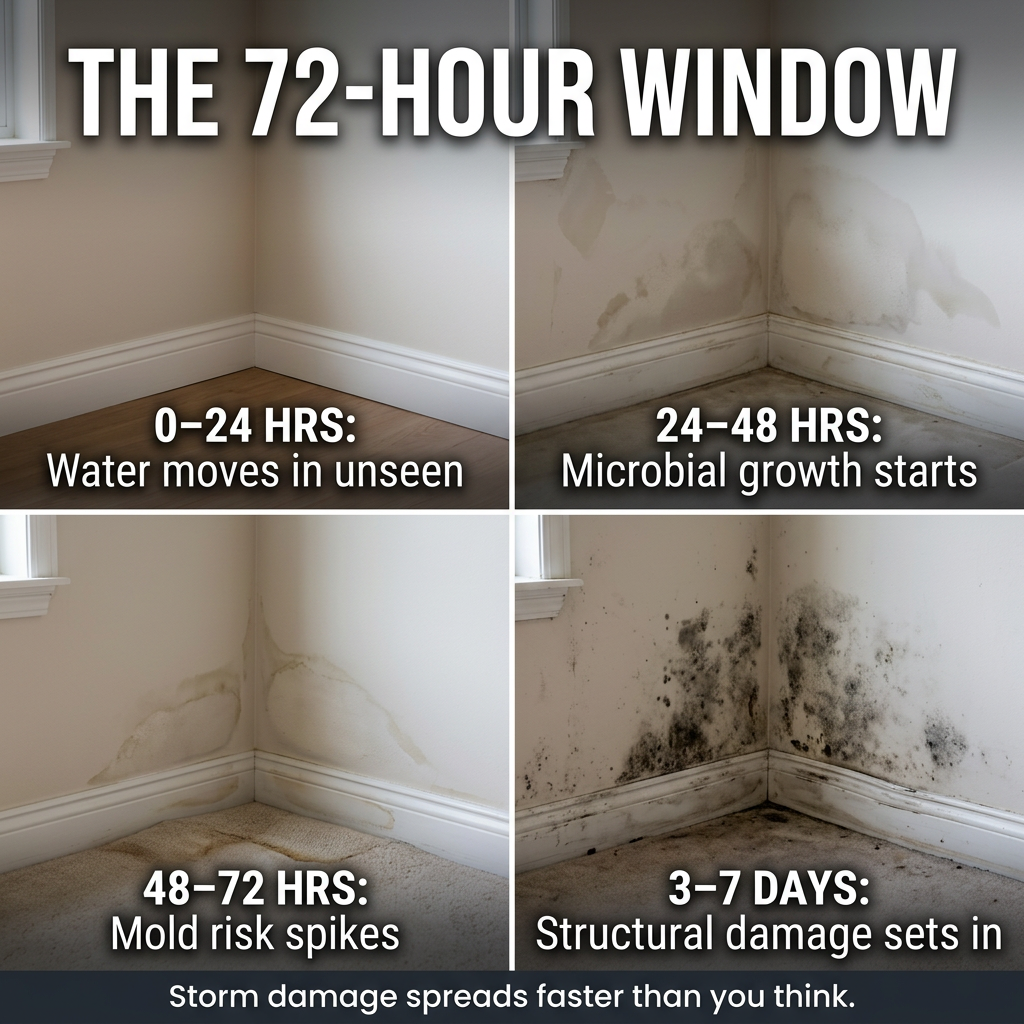

What happens in the first 72 hours after storm damage

Storm damage begins affecting your home immediately—and escalates significantly within the first 72 hours.

- 0–24 hours: Water penetrates drywall, flooring, and insulation. Materials absorb moisture beneath the surface. Electrical and structural risks begin forming.

- 24–48 hours: Microbial growth can begin. Odors develop. Porous materials like carpet padding become compromised.

- 48–72 hours: Mold risk increases significantly. Wood begins swelling and warping. Damage spreads beyond the original impact area.

- 3–7 days: Visible mold growth becomes likely in humid conditions. Structural materials degrade. Repair costs increase substantially.

Moisture doesn’t stay where it starts—it moves laterally and vertically through your structure. Learn about mold remediation services available for Newburgh homes and businesses.

How fast does storm damage lead to mold?

In humid environments like the Hudson Valley, mold growth can begin within 24–48 hours after water enters the home if materials remain wet. This is why early drying and moisture mapping are critical for Newburgh and Hudson Valley homes.

New York’s mold law often called Article 32 of the New York State Labor Law requires that mold projects over 10 square feet be handled by licensed assessors and remediation contractors who follow strict safety and documentation rules. As PuroClean of Poughkeepsie explains, proper, compliant mold remediation protects both indoor air quality and homeowners from liability and long‑term structural issues.

Why faster payouts don’t stop faster damage

Even if parametric insurance allows quicker access to funds, damage inside your home begins immediately and continues to spread. This is the gap most homeowners don’t see:

- Insurance (traditional or parametric) addresses financial recovery.

- Restoration addresses physical damage containment.

Those timelines do not align. Parametric insurance may accelerate payments but it does not slow down water, humidity, or mold growth.

Why immediate mitigation still matters regardless of insurance type

Acting quickly after a storm determines whether damage can be contained or becomes a full reconstruction. What starts as a small roof leak can:

- Spread into insulation, drywall, and flooring

- Travel behind walls and under surfaces

- Create hidden moisture pockets that worsen over time

The longer materials remain wet:

- The more likely they need to be removed instead of dried

- The higher the risk of mold and structural damage

- The more expensive the overall restoration becomes

Early action keeps damage localized. Whether your insurance payout is triggered by documented damage or storm data thresholds, the reality is the same, damage to your home begins immediately. Acting quickly to dry, clean, and stabilize affected areas is what prevents long-term issues like mold growth and structural deterioration.Give PuroClean of Poughkeepsie (845) 320-4646 and schedule a water and mold remediation assessment.

The hidden risk: delayed action costs more than delayed payouts

Waiting to act after a storm often causes more damage than waiting for insurance ever will.

Here’s the reality:

- Moisture doesn’t pause while claims are processed.

- Mold doesn’t wait for approvals.

- Secondary damage is what drives claim costs higher.

Scenario A — Waiting

Damage spreads unnoticed, materials become unsalvageable, mold risk increases, and repairs turn into reconstruction.

Scenario B — Immediate action

Moisture is detected early, materials are dried instead of replaced, damage stays contained, and costs remain controlled.

The difference isn’t the storm—it’s the response.

Why this matters specifically in Newburgh and the Hudson Valley

Local conditions in Newburgh make storm damage more likely to spread quickly and remain hidden.

- Spring and summer storms bring wind‑driven rain and high humidity.

- Winter ice dams cause delayed interior leaks.

- Older homes contain plaster, cavities, and layered materials that trap moisture.

- Finished basements hold moisture longer and hide damage.

These conditions create what’s known as delayed‑discovery damage—where problems worsen before they’re even visible.

When should you act after a storm

You should act immediately after any sign of storm‑related damage—waiting increases risk.

Take action if:

- You notice moisture or musty odors.

- You see staining on ceilings or walls.

- Your roof or siding took impact.

- Water entered the home at any level.

If water got in even slightly the clock has already started.

How PuroClean fits into the timeline of damage and recovery

PuroClean addresses the physical damage that begins immediately after a storm long before insurance processes are complete.

Whether your insurance payout is triggered by:

- Documented damage

- Or storm‑based data thresholds

…the reality is the same:

👉 Damage begins immediately, and early mitigation determines the outcome.

If your property experiences storm, water, or fire damage in Newburgh or the Hudson Valley, PuroClean of Poughkeepsie provides:

- Rapid response drying and dehumidification

- Moisture detection and containment

- Professional cleaning and restoration services

Final takeaway: insurance timing may change but damage timing doesn’t

Parametric insurance may change how quickly funds become available but it does not change how quickly damage spreads inside a home.

Storm data may influence payouts.

But your response in the hours after the event determines:

- The severity of damage

- The cost of repairs

- And whether restoration is possible or replacement is required

👉 Acting quickly isn’t optional—it’s what protects your property.

Frequently asked questions

What is parametric insurance in New York?

Parametric insurance is a type of coverage where payouts are triggered by measurable events like wind speed or rainfall, rather than only documented property damage. New York’s Insurance Law §1113 now recognizes parametric insurance for personal‑lines policies, including some homeowners and condo coverage in areas like Newburgh and the Hudson Valley.

Does parametric insurance replace homeowners insurance?

No. Parametric insurance is not a replacement for traditional homeowners insurance. It is usually a supplemental or additional layer of coverage that can pay out faster when storm data meets defined thresholds, but it does not cover all types of loss.

How fast does storm damage lead to mold?

In humid environments like New York, mold growth can begin within 24–48 hours after water enters the home if materials remain wet. This is why early drying and moisture mapping are critical for Newburgh and Hudson Valley homes.

Should I wait for insurance before starting restoration?

No. Waiting for insurance approval before starting restoration often allows damage to spread and can increase overall repair costs. Immediate mitigation helps protect your home and can support a smoother insurance claim, whether traditional or parametric.

What types of storm damage require immediate action in Newburgh?

Any water intrusion, roof damage, visible moisture, staining, or musty odors should be treated as an immediate concern. If wind, rain, ice, or debris has compromised your home’s exterior, contact a professional restoration service right away to inspect for hidden moisture.