You’ve just walked into your basement and found standing water creeping across the floor, or worse discovered a slow leak that’s been feeding mold behind your drywall for weeks. If you’re a homeowner in the Quad Cities area, Davenport, Rock Island, Moline, or Bettendorf, you know how fast the Mississippi River basin’s weather and aging home infrastructure can turn a normal Tuesday into a financial nightmare. The first question on your mind is almost certainly does homeowners insurance cover water damage? The honest answer is it depends and understanding the difference could save you tens of thousands of dollars.

This post breaks down exactly what’s covered, what’s excluded, how to file a water damage insurance claim in Iowa and Illinois, and what to do when your insurer won’t pay.

Homeowners insurance typically covers sudden and accidental water damage such as a burst pipe, failed appliance, or wind-driven rain entering through storm damage but does NOT cover flooding from external sources like rivers, storm drains, or surface water. For flood coverage, Iowa and Illinois homeowners need a separate flood insurance policy through FEMA’s National Flood Insurance Program (NFIP) or a private flood insurer. Maintenance-related water damage (slow leaks, seepage, or gradual deterioration) is also typically excluded. Coverage eligibility varies by policy; always contact your insurer immediately after a water damage event.

What Does Homeowners Insurance Actually Cover for Water Damage?

Standard homeowners insurance often called an HO-3 policy covers water damage that is sudden and accidental. In Iowa and Illinois, that generally means:

- A pipe that bursts due to freezing temperatures (common in Quad Cities winters)

- An appliance malfunction, such as a washing machine hose that fails unexpectedly

- Water that enters through a roof or wall after wind or hail damage often called a storm damage claim

- Accidental overflow from a tub, sink, or toilet

- Water discharge from a fire sprinkler system

If the damage meets these criteria, your insurer will typically pay for repairs to the structure, replacement of damaged personal property (under your contents coverage), and in some cases, temporary living expenses if the home becomes uninhabitable.

For a full breakdown of what the restoration process looks like after covered water damage, see our guide to water damage restoration in Davenport, IA & the Quad Cities area.

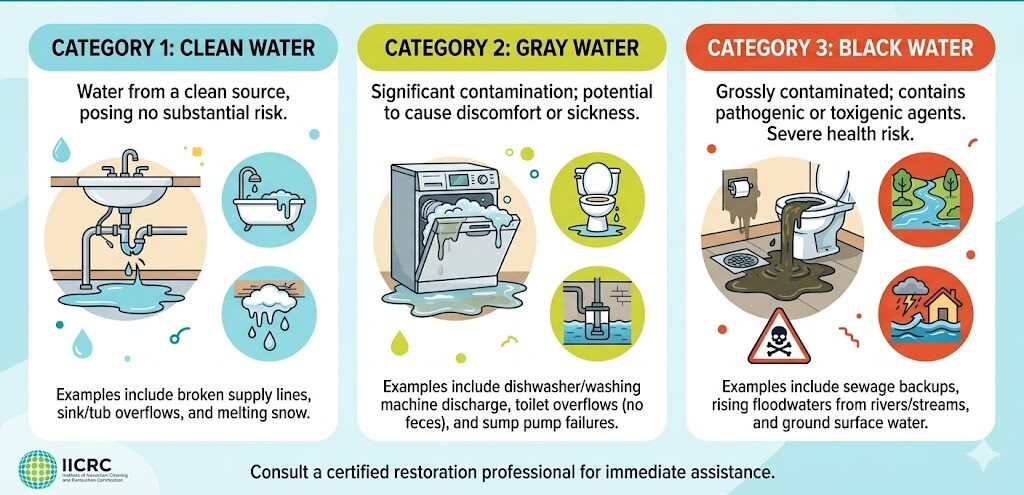

Coverage by Water Damage Category

Restoration professionals classify water damage into three categories under IICRC S500 standards:

- Category 1 (Clean Water): from supply lines, rain intrusion through a roof. Usually covered.

- Category 2 (Gray Water): from dishwashers, washing machines, sump pump failures. Coverage varies.

- Category 3 (Black Water): sewage backups, flooding, toilet overflows. Often excluded without a rider.

Does Homeowners Insurance Cover Water Damage from Flooding?

This is one of the most common and costly misunderstandings Iowa and Illinois homeowners face: standard homeowners insurance does NOT cover flooding.

| Flood insurance vs. homeowners insurance in Iowa: If water enters your home from outside, through a rising river, overwhelmed storm sewer, or surface runoff during heavy rainfall, that is legally defined as a flood. Your HO-3 policy will deny this claim. You need a separate NFIP flood insurance policy or a private flood policy to be protected. |

Scott County and Rock Island County both sit within or adjacent to FEMA-designated Special Flood Hazard Areas (SFHAs). Homeowners in these zones who carry a federally backed mortgage are required by law to hold flood insurance. But even homeowners outside of high-risk zones are increasingly experiencing flood damage, the Quad Cities area has seen repeated significant flooding events tied to Mississippi River surges and rapid snowmelt.

The Iowa Insurance Division and the Illinois Department of Insurance both recommend that homeowners review their policies annually and specifically ask their agent whether their property sits in a flood zone. FEMA’s flood maps are updated regularly, and your zone designation may have changed.

Does Homeowners Insurance Cover Water Damage from Sewer Backup?

Sewer backup and sump pump failure are not covered under a standard Iowa or Illinois homeowners policy but they can be added as an endorsement (rider) for a relatively low additional premium. In the Quad Cities, aging municipal sewer infrastructure in Davenport, Moline, and Rock Island makes sewer backup one of the most frequent causes of basement flooding and mold growth.

If your sump pump fails during a heavy rain event and water floods your finished basement, your base policy will likely deny the claim. With a sewer backup endorsement, you may have up to $10,000–$25,000 in coverage, depending on your insurer.

What Water Damage Does Homeowners Insurance NOT Cover?

Beyond flooding and sewer backup, there are several common exclusions homeowners in Iowa and Illinois are often surprised to discover:

- Gradual leaks: A slow drip under a sink that causes mold over months is considered a maintenance issue, not an accident.

- Seepage or groundwater: Water migrating through foundation walls or basement floors is excluded.

- Neglect: If you knew about a leak and didn’t address it, the insurer can deny the claim on the basis of neglect.

- Mold resulting from excluded events: If the underlying water source isn’t covered, the mold it causes typically isn’t either.

- Earth movement: Water damage caused by soil movement or settling is excluded.

This last point about mold is critical. Mold remediation following a covered water loss can sometimes be added to your water damage insurance claim, but insurers frequently try to minimize this payout. Proper documentation by an IICRC-certified restoration company like PuroClean of Davenport is essential to substantiate your claim

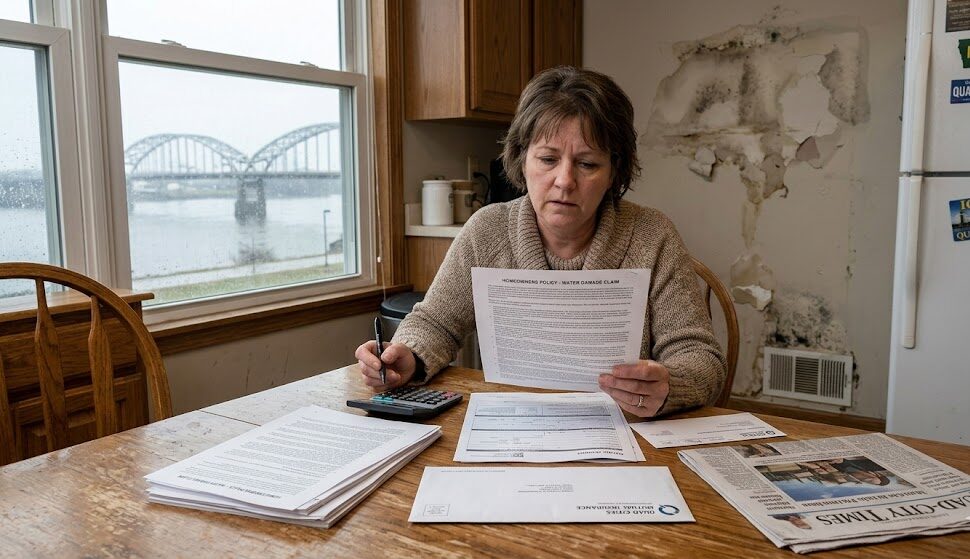

How to File a Water Damage Insurance Claim in Iowa or Illinois

Acting quickly and documenting everything is the key to a successful water damage insurance claim. Here’s the process:

- Stop the source: Shut off water to the affected area if possible.

- Document everything: Photograph and video all damage before any cleanup begins.

- Call your insurer: Most policies require prompt notification, waiting can jeopardize your claim.

- Begin emergency mitigation: Under most policies, you are required to take reasonable steps to prevent further damage. This is where a 24/7 restoration company is essential.

- Get a written restoration estimate: An IICRC-certified company’s written scope of work carries significant weight with adjusters.

- Meet your adjuster: Walk them through the damage with documentation in hand.

- Review the settlement offer: If it seems low, you have the right to dispute it with additional documentation.

Don’t wait to act. The first 24 hours after water damage are the most critical. Read our full guide: What to Do in the First 24 Hours After Water Damage, step-by-step guidance for Quad Cities homeowners.

Does Homeowners Insurance Cover Mold After Water Damage?

Mold coverage is one of the most contested areas of homeowners insurance in Iowa and Illinois. The general rule: if the mold grew as a direct result of a covered water loss event, remediation may be covered, subject to a sublimit (often $5,000–$10,000 on standard policies). However, if mold developed due to an excluded event, like long-term seepage or flooding, the insurer will deny mold coverage as well.

This is why proper documentation of the timeline when the water event occurred, when damage was discovered, and when mitigation began is so important. PuroClean of Davenport’s IICRC-certified technicians follow IICRC S520 mold remediation standards and provide detailed written assessments that support insurance claims.

Does Homeowners Insurance Cover Storm Damage Water Intrusion?

When a severe storm causes direct physical damage to your roof, siding, or windows and rainwater then enters through the breach, that water damage is typically covered under your homeowners policy as part of the storm damage claim. This is sometimes called wind-driven rain coverage. However, there’s a critical distinction: if your roof was already in poor condition before the storm and an adjuster determines that the damage is partly attributable to deferred maintenance, your claim may be reduced or denied. Quad Cities homeowners dealing with storm season should proactively document the condition of their roof and exterior

Water Damage in Your Quad Cities Home? PuroClean of Davenport Is Here 24/7

Navigating a water damage insurance claim is stressful enough without having to worry about whether the damage is getting worse every hour. PuroClean of Davenport is the Quad Cities area’s trusted IICRC-certified restoration company, serving Milan, Davenport IA, Bettendorf, Rock Island, Moline, and surrounding Scott County and Rock Island County communities.

Here’s why property owners throughout Iowa and Illinois choose us:

- IICRC-certified technicians following S500, S520, and S700 restoration standards

- 24/7 emergency response: we arrive fast to stop damage before it spreads

- Direct coordination with your insurance adjuster to document and support your claim

- PuroClean’s insurance assistance process ensures nothing falls through the cracks

- Comprehensive services: water extraction, structural drying, mold remediation, and full restoration

📞 Call PuroClean of Davenport Now for a Free Emergency Assessment

Don’t wait, every hour matters when water damage occurs. Our team is ready to respond, document your loss, and work directly with your insurer. Call us on (563) 484-4846 or Request Your Free Assessment

Frequently Asked Questions

Does homeowners insurance cover water damage from a burst pipe?

| Yes. A burst pipe that causes sudden and accidental water damage is covered under standard Iowa and Illinois homeowners insurance policies. The damage to your home’s structure and your personal belongings may both be covered, subject to your deductible. You are responsible for the cost to repair the pipe itself. |

Does homeowners insurance cover water damage from flooding in Iowa?

| No. Flooding from external sources — including river overflow, storm surges, and surface water — is not covered by standard homeowners insurance in Iowa or Illinois. You must purchase a separate flood insurance policy through FEMA’s NFIP or a private insurer. Scott County and Rock Island County homeowners in FEMA flood zones may be required to carry flood insurance by their mortgage lender. |

How do I file a water damage claim with my insurance company?

| Contact your insurance company as soon as possible after the damage occurs. Document all damage with photos and video before cleanup begins. Engage an IICRC-certified water damage restoration company immediately to begin emergency mitigation, as most policies require you to prevent further damage. Your restoration company’s written assessment will support your adjuster’s review. |

Does homeowners insurance cover mold remediation in Illinois?

| Mold remediation may be covered if the mold directly resulted from a covered water loss event, such as a burst pipe or storm damage. Most Illinois homeowners policies include a mold sublimit, commonly $5,000–$10,000. Mold resulting from flooding, long-term seepage, or neglect is typically excluded. |

What is the difference between flood insurance and homeowners insurance?

| Homeowners insurance covers sudden and accidental internal water damage (burst pipes, appliance failures, storm-breached roofs). Flood insurance, issued through FEMA’s NFIP or private insurers, covers water damage caused by external flooding events — rising rivers, storm drains, and surface water runoff. You need both policies to be fully protected in the Quad Cities area. |