As water damage restoration specialists at PuroClean of Ft. Lauderdale South, we’ve seen the devastation floods can cause—soggy carpets, warped walls, and cherished belongings ruined.

From Fort Lauderdale to Pembroke Pines and Hollywood, we’ve helped countless homeowners recover from floods, and one thing stands out: flood insurance is often the difference between a swift recovery and financial disaster.

Flooding is the most common and costly natural disaster in the U.S., with 90% of presidentially declared disasters involving floods.

Standard homeowners insurance doesn’t cover flood damage, leaving many unprepared. In this comprehensive guide, we’ll dive into everything you need to know about flood insurance, drawing from authoritative sources like the National Flood Insurance Program (NFIP), FEMA, and others.

We’ll cover what flood insurance is, why it’s critical, what it covers, how to assess your risk, and practical steps to prepare and recover—ensuring you’re ready when waters rise.

Table of Contents

What Is Flood Insurance? A Restoration Expert’s Perspective

Flood insurance is a specialized policy that covers losses from flooding, defined as an excess of water on normally dry land affecting two or more acres or properties. This could stem from a hurricane in Miami, a burst pipe in Davie, or heavy rains overwhelming drainage in Pembroke Pines.

Unlike homeowners insurance, which covers fire or theft, flood insurance is tailored for water-related disasters. At PuroClean, we’ve seen how vital it is for homeowners to have this coverage to fund professional restoration after a flood.

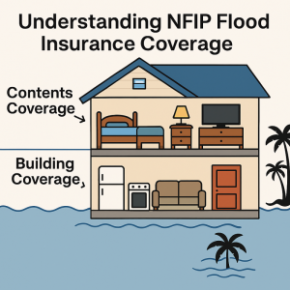

The NFIP, managed by FEMA, provides flood insurance through private insurers in over 22,600 participating communities nationwide[1]. Available to homeowners, renters, and businesses, policies typically have a 30-day waiting period, so don’t wait for a storm warning to act. The two main coverage types are:

Building Coverage:

Protects your home’s structure—foundation, walls, electrical/plumbing systems, HVAC, and built-ins like cabinets—up to $250,000 for residences.

Contents Coverage

Covers personal items like furniture, electronics, and clothing, up to $100,000, with limited basement coverage for essentials like sump pumps.

Premiums, averaging $786/year, vary by location, elevation, and coverage amount. In high-risk areas like parts of Hollywood, costs may be higher, but low-risk zones like some Pembroke Pines neighborhoods can see premiums as low as $400.

As restoration experts, we know insurance makes our job—restoring your home—faster and less stressful.

Why Flood Insurance Is Non-Negotiable

We’ve worked on countless flood-damaged homes, from small leaks to major inundations, and the story is always the same: uninsured homeowners face massive challenges.

Standard homeowners policies exclude flood damage, and repair costs can soar—$25,000 for just an inch of water. Federal disaster aid, when available, averages only $5,000 and often requires repayment. Flood insurance bridges that gap.

Flooding isn’t just a coastal issue. Nearly one-third of NFIP claims come from low- to moderate-risk areas. In South Florida, heavy rains, poor drainage, or urban development can trigger floods anywhere. Here’s why flood insurance is critical:

Swift Recovery:

Covers professional restoration services, like our IICRC-certified water extraction and drying, saving you from out-of-pocket costs.

Mandatory in High-Risk Areas:

Federally backed mortgages in flood zones require it.

Climate Risks:

Increasing hurricanes and sea-level rise make flooding more likely, even in “safe” areas like Davie.

Community Benefits:

NFIP participation encourages floodplain management, reducing future risks.

Hurricane season, a focus of FEMA’s campaigns, heightens the urgency. We’ve restored homes hit by storms like Tropical Storm Chantal, and insured clients always recover faster.

What Flood Insurance Covers (and What It Doesn’t)

When we arrive at a flooded home in Dania Beach, insurance coverage shapes our restoration plan. NFIP policies cover direct physical losses from flooding, but details matter. Here’s what’s included:

Building Coverage:

Foundations, walls, electrical/plumbing, HVAC, built-in appliances, and permanent carpeting.

Contents Coverage:

Furniture, electronics, clothing, portable appliances, and valuables (up to $2,500 unless enhanced).

Sewer backups caused by flooding are covered, but exclusions apply:

- Outdoor property (decks, patios, pools).

- Basements (limited to essentials; finished walls or furniture aren’t covered).

- Mudslides or earth movement.

- Vehicles or currency.

For example, if your Fort Lauderdale home floods, your policy might cover water-damaged drywall but not your outdoor pergola. Our team uses advanced tools like thermal imaging to detect hidden moisture, ensuring claims cover all damage, like potential mold growth within 24 hours.

Assessing Your Flood Risk: Tools and Insights

Understanding your risk is step one. The FEMA Flood Map Service Center is a must-use tool—enter your address to see if you’re in a high-risk Special Flood Hazard Area (1% annual flood chance), moderate-, or low-risk zone. High-risk areas have a 26% chance of flooding over a 30-year mortgage.

In South Florida, areas near Fort Lauderdale Airport or Hard Rock Hotel often face higher risks due to low elevation or proximity to canals.

Other ways to gauge risk:

Historical Data:

Check FEMA’s disaster records for past floods in your area.

Elevation

Homes below the Base Flood Elevation (BFE) are pricier to insure.

Local Factors:

Urban growth in Pembroke Pines can disrupt drainage, increasing risks.

Climate Trends:

Rising sea levels and intense storms are growing concerns in Miami-Dade.

Even in low-risk zones, where premiums are affordable, insurance is a smart move. We’ve seen clients in “safe” Hollywood neighborhoods regret skipping it after flash floods.

How to Get Flood Insurance: A Simple Roadmap

Ready to protect your home? Follow these steps:

- Check Your Risk: Use FEMA’s Flood Map Service Center.

- Get a Quote: Visit Floodsmart.gov or contact an NFIP insurer.

- Choose Coverage: Select building and/or contents coverage; consider endorsements for valuables.

- Purchase: Work with an agent to finalize.

- Prepare: Account for the 30-day wait and take preventive measures (below).

Costs vary—low-risk areas start at $400/year, while high-risk zones like parts of Miami may exceed $1,000. Community discounts or mitigation efforts can lower premiums.

Expert Recommendations for Flood Preparation and Recovery

At PuroClean of Ft. Lauderdale South, we specialize in water damage restoration, and our experience informs these practical tips to minimize flood damage and recover effectively:

Before a Flood:

- Elevate appliances (e.g., water heaters) above the BFE.

- Install sump pumps and backflow valves to prevent sewer backups.

- Store valuables in waterproof containers on upper floors.

- Improve landscaping to direct water away from your home.

- Review your policy annually with an agent to ensure adequate coverage.

During a Flood:

- Stay safe—follow local alerts (e.g., for Tropical Storm Chantal).

- Turn off electricity if safe.

- Avoid floodwaters due to contaminants or electrical risks.

After a Flood:

- Contact your insurer immediately to file a claim (see Floodsmart.gov’s recovery guide).

- Call PuroClean at (754) 732-8383 for 24/7 emergency water extraction to prevent mold, which can form in 24 hours.

- Document damage with photos for claims.

- Avoid DIY cleanup—biohazards and hidden moisture require professional tools like our HEPA filtration systems.

Mitigation, like elevating structures, can also lower premiums and risks, as seen in FEMA’s community programs.

Real Stories: The Impact of Flood Insurance

In Londonderry, Vermont, business owners rebuilt after Tropical Storm Irene using NFIP insurance and FEMA grants. One owner noted, “You can’t live without flood insurance near the river.” In South Florida, we’ve seen similar stories.

A Pembroke Pines client faced a flooded laundry room from a pipe burst; their insurance covered our rapid restoration, saving them $20,000. Without it, they’d have faced crippling costs. These cases show why preparation and professional remediation are key.

Hurricane Season: Act Now

Hurricane season, highlighted by FEMA, brings heightened flood risks. Storms like Chantal can dump inches of rain in hours, especially in Miami or Dania Beach. Stock an emergency kit, monitor alerts, and ensure your policy is active. Our 24/7 team is ready to respond, but insurance ensures a smoother process.

Busting Flood Insurance Myths

Myth: “I’m not in a flood zone, so I don’t need it.”

Fact: 32% of claims are from low-risk areas.

Myth: “Homeowners insurance covers floods.”

Fact: It doesn’t.

Myth: “It’s too expensive.”

Fact: Many pay less than $500/year.

Myth: “Federal aid will save me.”

Fact: Aid is limited and often a loan.

Conclusion: Protect Your Home Today

Floods don’t discriminate, but with insurance and expert restoration from PuroClean of Ft. Lauderdale South, you can recover faster. Visit Floodsmart.gov, get a quote, and call us at (754) 732-8383 if disaster strikes. Don’t wait—protect your home now.

Sources: